After spending three years and over 10,000 hours researching and studying reports by the private and public sectors on financial and entrepreneurship education, the team at Life Hub is ready to launch what it believes a revolutionary step in childhood education and financial literacy.

The research they conducted overwhelmingly points to a societal issue, Financial Illiteracy. At the root of this problem is experience, education and knowledge. The solution, surprising to many, is not taught in a classroom, but rather experiential learning on a daily basis, utilizing real monetary assets, starting as early as age 3.

Their research also showed positive or bad behaviors exist in us regardless of wealth because behaviors are formed between the ages 7-9. If the appropriate exposure and effective training are missed during the years leading up to that age, chances are the individual won’t possess positive behaviors as an adult. So, what is a solution?

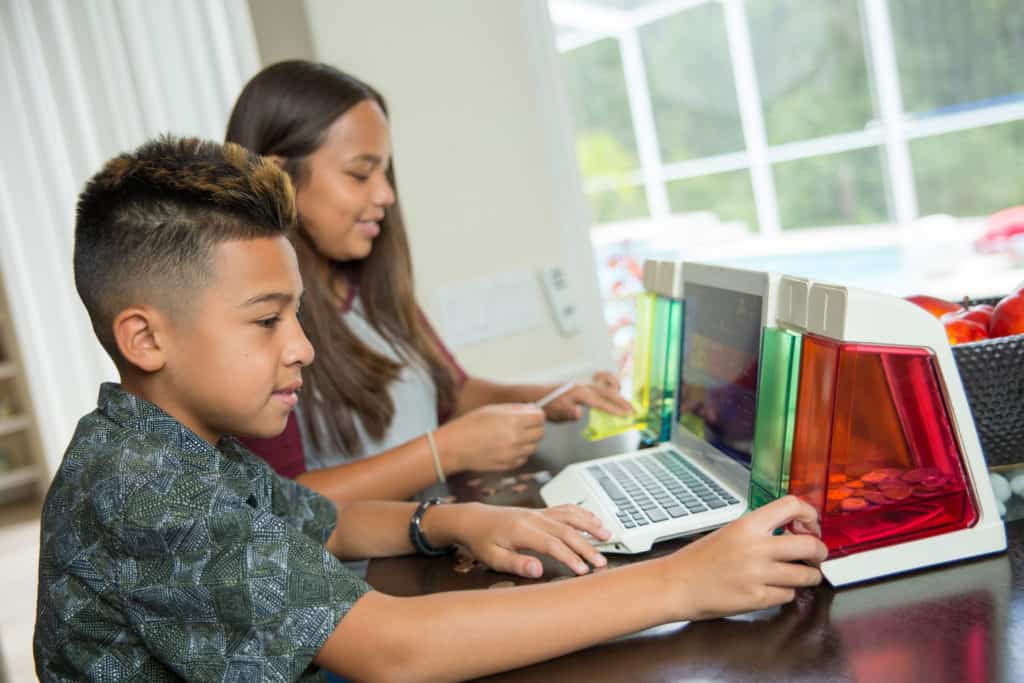

The team believes it’s their patented technology platform, Life Hub. The platform incorporates a comprehensive suite of software modules that touch many aspects of life management including banking, investing, shopping, chores, entrepreneurship, and business.

Children ages 3-14 learn how to transact their lives responsibly via Life Hub’s Eco-system of modules. Life Hub is a home-based integrated hardware and software system that keeps family members connected and engaged to manage vital aspects of everyday life.

The eco-system encourages family participation and helps parents expose and teach their children about financial management without feeling they need to be the expert.

Below is an interview with John Seib, Partner at Electus Global Education Co.(the maker of Life Hub).

Q: What inspired the Life Hub to be created?

Although financial literacy is one of the most critical social and economic issues of our time, current methods being used to engage and teach children’s financial and money management skills have been in large part unsuccessful.

Although our entire industry is sufficiently developed and is ultimately cognizant of the bona fide educational solutions to the problem, it has failed and continues to fail to institute, implement and apply those solutions that effectively achieve the desired results.

With the recognition of our industry’s failures, our team simply asked, “Why is an entire industry, which is so vital to improving the quality of life in the US and around the world, failing when the educational methodologies for the solutions are not only well-known but acknowledged and available for it to practice?”

Through the inspiration of addressing and finally fixing one of today’s most critical social and economic problems, our team committed 3 years and more than 10,000 hours of research and development to identifying and understanding those educational failures.

Isolating, extracting, and mapping out the deficiencies and shortcomings on an individual basis that ultimately contribute to the overall failure. We began with a clean sheet of paper, aligning each element of those educational deficiencies and then recalibrating, augmenting and upgrading them with psychologically and scientifically proven educational methodologies that ultimately deliver effective learning solutions to achieve the desired results.

In our R&D phase, our team innovated, designed, developed and manufactured an integrated stand-alone home-based (IoT) education technology. Our platform solves this critical global problem at the heart of where it truly needs to be solved, at the early childhood development years where positive behaviors and habits can be formed between the ages of 7 to 9.

Our globally patented home-based education technology zeros in on what really matters and effectively engages children at the youngest possible age, as early as 3. Children handle and manage real and tangible monetary assets at home, every day which, is paramount to effective and lasting outcomes.

Industry Status Quo

Today, our industry is generally characterized by four educational processes and methodologies:

- Classroom-based courses and curriculums in schools

- Digital and web-based courses and programs

- Financial management mobile applications

- Online and app video educational games.

School Courses

The predominate method of teaching children financial skills today is through academic/school(knowledge-based) courses and curriculums. Students are provided a financial literacy course over a semester and then tested at the end of the course to determine and quantify knowledge acquisition.

Studies show knowledge-based education alone has little effect and impact on positive financial behavior formation and therefore on making children meaningfully financially capable over the long-term.

Digital and Web-based Programs

Like knowledge-based education in schools, digital and web-based courses alone are ineffective at forming positive money behaviors in children.

Financial Management Mobile Applications

Mobile apps can be useful utilities and tools for managing money and finances for older teens and adults who have already formed and acquired the positive behaviors and skills needed to do so effectively.

However, they are ultimately ineffective and inadequate at educating young children financial and money management skills. Principally because managing digital or invisible money is altogether unconducive to the formation of positive behaviors and habits, critical to achieving lasting outcomes and results.

A recent study articulates how mobile financial technology is inducing overspending and mismanagement of money and finances endangering financial wellbeing. It demonstrates and reinforces the perils of managing invisible money by those who have not first learned, acquired and formed the necessary skills and positive behaviors for the effective management of real money.

Today there are numerous entities in the marketplace with financial management and mobile app technologies. Representing themselves to be tools for effective financial education for children. We would argue against the validity and veracity of invisible money being utilized as the means for effectively teaching children financial skills and behaviors.

Online and Mobile App Video Games

Studies show that online and mobile app video games for youth financial education, particularly numeracy games and stock market games, can certainly serve as useful and effective tools to acquire certain digital skills with children. However, video games incorporate only digital presentation or proxies of actual money and there is no evidence or research that proves that video games contribute to or induce positive behavior formation with children.

Ultimately, there is no such thing as “bad youth financial education”. Any industry product or service that shines a light on the matter is positive for families and communities. However, the fragmented nature of the industry and its vast assortment of products and services can be quite confusing.Marketing declarations from providers claiming their technologies are effective tools at achieving positive behavior formation and therefore financial capable children, are contrary to published research of studies, facts and figures. This can provide a false sense of security to parents, to the detriment of their children.

Educational providers delivering a semester course of financial literacy or a 5-hour online digital program to children and then declaring them financially literate and capable, may convey to parents a false narrative. Believing their children have acquired the vital behaviors and skills necessary. The reality is to achieve true financial literacy and capability, children must engage frequently and consistently both with knowledge-based and practical-based learning over many years to truly acquire these vital skills and behaviors. Well informed parents are key to transitioning the nation’s future generations into financially capable adults.

Q: Can you give us an idea of what the Life Hub does compared to a normal laptop?

From the outset of our venture we were faced with a decision. To embark on an entrepreneurial journey towards truly addressing and fixing this critical problem or build and launch yet another me-first product quickly and inexpensively.

In 2015, despite knowing the efforts, time and resources needed to tackle this problem, our team chose to form the organization that would ultimately deliver the industry’s most powerful and comprehensive technological solution for youth financial and entrepreneurship education. A solution that could address and fix the problem at its root cause.

“Our DNA is firmly embedded in our thesis that the current global financial illiteracy epidemic is one of the most critical social and economic issues of our time.“

John Seib, Partner at Electus Global Education Co.(the maker of Life Hub).

That addressing and curing this epidemic with the most effective means and technology is vital to the wellbeing of societies worldwide.

Life Hub is the world’s most advanced youth financial and entrepreneurship education technology. It’s the first home based all-in-one computer system, specifically designed to engage and teach children aged 3 to 14 financial, money management, entrepreneurship, and life management skills. Life Hub empowers them to manage real monetary assets and businesses on a daily and consistent basis and learn by “failing” in a safe environment.

Forming positive money behaviors at a young age is critical to a child’s success later in life. Life Hub is a purpose-built technology designed for positive behavior and habit formation.

Life Hub is based on 3 key principles.

- First, it’s a technology designed to engage children as young as age 3 so that positive behaviors can be ingrained by their teen years.

- Second, positive money and entrepreneurial habits are best formed by managing real money and business every day at home using advanced practical hands-on technology. Life skills and entrepreneurial spirits are best taught, nurtured and continually reinforced at home beginning at an early age.

- Third, the engagement and learning are individualized, frictionless, age-appropriate and fun. Children are learning the right financial, entrepreneurial and life skills at the right age in an effortless and enjoyable way.

Q: Do you develop the apps/programs in house that go on the Life Hub, or are 3rd party developers?

We are a full stack enterprise and therefore design, develop and completely control the entire user experience. Other than the operating system, we design and manufacture all elements of our fully integrated technology including the hardware, software, mobile application and educational content.

Life Hub incorporates an ecosystem of 23 primary financial, entrepreneurship and life management modules. 22 of the modules are experiential engagement and learning modules designed to be native or exclusive to Life Hub. Life Hub’s 23rd module is Life Academy. The only non-experiential engagement module on the system. Life Academy is designed to host the industry’s highest quality knowledge-based products and services predominantly from top third-party industry providers. Including financial literacy and entrepreneurship courses, programs, curriculums, books, comics, videos, industry facts and figures, digital and web-based courses, educational video games, educational apps, event and camp organizers, all beautifully curated and organized. Children and parents have fingertip access to these top-rated products and services.

Life Hub also deploys A.I. to analyze children’s profiles, learning skills and abilities. Providing the ability to make recommendations as to which knowledge-based learning products and services are most suitable and appropriate for them at various ages and stages. Another industry first.

Q: What do you foresee kids and families valuing the most out of the Life Hub platform?

At a time when financial education is becoming increasingly important, the physical connection to money is becoming weaker. Teenage children are buying more stuff online and in digital stores, but don’t know how these transactions work or how money underpins them. The costs are becoming abstract, creating a real societal problem.

When children are divorced from the real financial cost of a transaction and don’t see and feel the pain associated with the loss of money resulting from the exchange of the money for purchases, it becomes harder for them to get their heads around what things cost. That repeated behavior is likely to lead them to overspend and consume more and consume mindlessly. They see this invisible money as an abstract and unlimited resource rather than real money coming in and out of their possession and bank accounts.

Life Hub’s central purpose is to engage young children with real money and finances on a daily and consistent basis using its suite of modules, so they acquire the skills and form positive money behaviors. Preparing them to transact their lives responsibly with invisible money on mobile technology as they reach their teen and adult years.

The platform has 23 integrated easy-to-use financial, money management, entrepreneurship, and life management software modules that are all age appropriate. Life Hub’s suite of 23 primary and more than 195 secondary and tertiary modules empower children aged 3 to 14 to manage real money, business and their lives at home every day.

While Life Hub provides children with the broadest and most comprehensive scope of engagement and learning modules. The nucleus modules are Deposit, Withdraw, Banking, Investments, Shopping, Charities and Business. Ultimately, its these modules that empower children to manage real money through earning, saving, investing, spending and donating activities and engagements. All foundational skills and behavior developments for financial education.

Q: How much does the Life Hub costs and when will it be available for families to purchase?

Life Hub can be purchased for a monthly payment of $ 14.99, paid over 36 months. Children engage with and utilize Life Hub to earn, save, allocate and pay the small monthly payments on time every month themselves. This serves as a teachable moment.

Since Life Hub is a home-based shared and communal technology for the entire family, serving up to 4 children in the household, every child becomes responsible for their portion of the monthly payment. With 3 pre-teen children in the household, the monthly payments will be only $ 5 a month per child.

The monthly payments for the Life Hub purchase serve as a terrific way for children to learn how to manage money and finances as well as learn personal responsibility. Establishing the habit of fulfilling and meeting financial commitments and obligations in a timely and trustworthy way.

Family households can also apply for our “Hub for Every Child”. An initiative whereby they receive cost-free Life Hubs.

In collaboration and partnership with our non-profit foundation arm, Electus Life Education Foundation and benefactors, we manufacture and distribute Life Hubs to family households with young children at no cost them.

We anticipate commencing the manufacturing and distribution of Life Hub in second quarter of 2020.

Q: How would you like to see Life Hub continue to grow in the future?

Looking forward to years after market launch. Our ground-breaking education technology is installed, utilized and has become a vital component of the family household much like televisions and PCs. Entire families converging to interact, create, build and learn in millions of households across the globe. We are witnessing the transition of millions of children into financially capable and entrepreneurial adults whose lives have been positively altered and transformed because of Life Hub.

The most significant impact we hope to witness is Life Hub becoming a powerful catalyst for equality of opportunity, social justice, economic empowerment and educational equivalence for all children in the United States and across the globe.

Related post: Codeverse Expands its Interactive Coding Studio for Kids Across the Country

Latest Posts:

- Meet the World’s First Green Digital Asset, a Carbon Credit-Backed Token

- Investment Banker Turned Social Entrepreneur Left his Career to Design Innovative Clothing for Cancer Patients

- The Journey to Create a New Standard of Mental Wellness Through Unique Psychedelic Therapeutics and Treatment

- Brixilated Created a Mindfulness Curriculum That Uses Lego® to Help Individuals With Their Opioid Recovery Journey

- Investing in Regenerative Agriculture and the Future of Farming

Access Rights | Content Availability:

Access Rights | Content Availability:

APU Content Aggregation Service

APU Content Aggregation Service